Official WeChat

Building Materials Industry Prosperity Index (MPI) for September 2025

PublishDate:2025-11-18

Source:CNBM Official Website - News Center

I. Building Materials Industry Prosperity Index for September

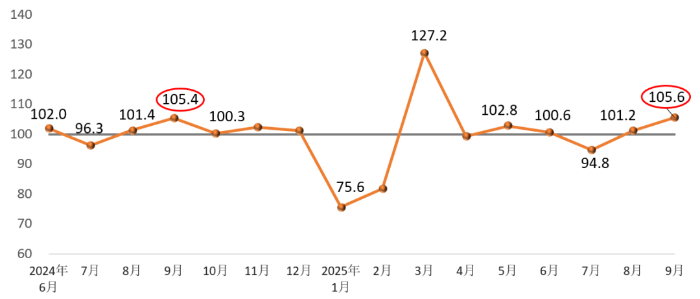

In September 2025, the Building Materials Industry Prosperity Index stood at 105.6 points, above the critical threshold and within the prosperity range. This represents an increase of 4.4 points compared to August and is 0.2 points higher than the same period last year, indicating a continued recovery trend in the building materials industry.

Monthly Building Materials Industry Prosperity Index

On the supply side, in September:

- The Building Materials Industry Price Index was 99.8 points, up 0.8 points from the previous month but still below the critical threshold.

- The Building Materials Industry Production Index was 105.8 points, up 3.6 points from the previous month, remaining above the critical threshold.

Overall, prices of building materials products continued to decline compared to the previous month, but the rate of decline narrowed. Production activity in the building materials industry improved compared to August.

On the demand side, in September:

- The Building Materials Investment Demand Index was 106.4 points, above the critical threshold and up 6.3 points from the previous month, indicating continued recovery in investment-related markets.

- The Building Materials Industrial Consumption Index was 104.5 points, above the critical threshold and up 2.1 points from the previous month, reflecting sustained recovery in demand from manufacturing sectors that utilize building materials products.

- The Building Materials International Trade Index was 98.4 points, down 0.4 points from the previous month and below the critical threshold, signaling a decline in the value of foreign trade for building materials compared to August.

Overall, investment demand and industrial consumption demand showed steady growth in September, while international trade demand experienced an adjustment and slight decline.

II. Analysis and Early Warning of MPI Influencing Factors

Accelerated Production of Building Materials Products

In September, although new construction in the real estate sector remained generally weak, the easing of climatic factors such as high temperatures and heavy rainfall, combined with coordinated macro-policy support, led to a recovery in demand from downstream manufacturing sectors. As a result, building materials production accelerated compared to July and August. All 13 sub-sectors of the building materials industry recorded production indices within the prosperity range. Notably, industries such as wall materials, clay and sand mining, construction stone, and mineral fibers and composite materials saw a more pronounced recovery in production activity compared to the previous month.

Narrowed Decline in Factory Prices of Building Materials Products

In September, among the building materials sub-sectors:

- Eight industries—including waterproof materials, lightweight building materials, lime and gypsum, clay and sand mining, construction stone, mineral fibers and composite materials, architectural sanitary ceramics, and non-metallic minerals—experienced month-on-month price increases, five more than in August.

- Three industries—cement, concrete and cement products, and wall materials—recorded month-on-month price declines.

Factory prices of products in three industries—clay and sand mining, construction stone processing, and architectural sanitary ceramics—maintained year-on-year growth. Overall, building materials prices continued to fluctuate at low levels, though the decline narrowed.

Cautious Assessment of Market Expectations

Since September, the macroeconomic environment has shown signs of stabilization and improvement, bolstered by expectations of interest rate cuts, which have positively influenced sentiment among building materials enterprises. However, according to data from the National Bureau of Statistics:

- From January to August, national fixed-asset investment in construction and installation engineering decreased by 2.2% year-on-year, with the decline widening, while infrastructure investment grew by 2.0% year-on-year, though at a slowing pace.

- Production growth rates for products such as automobiles, electric multiple units (EMUs), solar batteries, and electronic appliances have slowed.

Demand in the building materials market remains relatively weak, necessitating cautious evaluation of market expectations. Recently, prices of fuels such as coal and natural gas have declined, which is favorable for reducing costs for building materials enterprises.